Liquidity – the ability to convert assets into cash – generally worries investors.[1] In talking with clients and in my forestry investment research, I find that the issue of liquidity varies significantly by investor and over time, and that we are quick to generalize about the advantages and disadvantages of liquidity. How can we frame liquidity in a way that provides context for planning and decision-making?

Issues Related to Liquidity

In finance, liquidity is a construct that affects certain folks in certain situations; it does not affect everyone always. Liquidity, a problem when you need it and don’t have it, covers issues that may relate or overlap. For example, consider the use of debt (leverage) and the valuation of assets.

Debt differentiates during market crashes. While leverage has its role in finance, investors without debt will be less compelled to liquidate during tough markets. For highly leveraged organizations, debt compresses time and reduces options.

If we view liquidity as a balance of buyers and sellers at any time, then in the absence of buyers or sellers, how do we value an asset? When traders scramble to pay debts and meet margin calls, they don’t sell what they should, they sell what they can. Investors in comparable situations act surprised when markets tank and buyers are nowhere to be found.

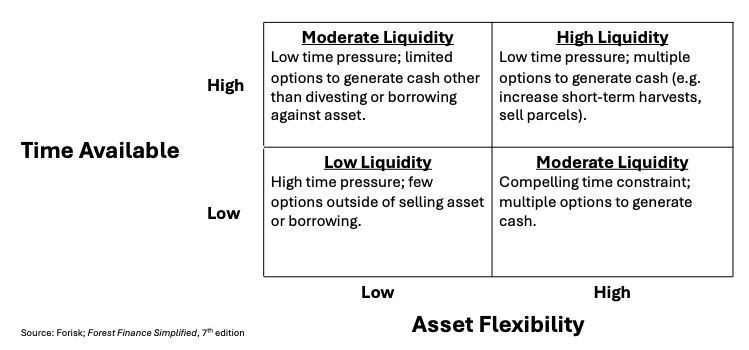

Plan Ahead to Manage Liquidity

At times, investors need cash. In forestry, for example, due to irregular harvest revenues on smaller timberland ownerships, an investor may need supplementary funds through a partial sale, an advance, or a loan. While situations require balancing time with flexibility, it helps to plan how one might unload a timberland tract in a crisis. Investors get part-way there by breaking down the forest into its salable components, including timber, hunting rights, and choice parcels.

At the Federal Reserve Bank’s 2005 Jackson Hole Economic Policy Symposium in Wyoming, economist Raghuram G. Rajan, then working with the IMF, noted how actual and perceived time pressure from excessive debt, unusual financial structures, or other obligations can essentially manifest losses through illiquidity. He observed[2]:

Liquidity allows holders of financial claims to be patient… and allows the value of the net financial claim to more fully reflect fundamental real value. Not only does illiquidity perpetuate the overhang of financial claims as well as uncertainty about their final resolution, a perception of too little aggregate liquidity in the system can trigger off additional demands for liquidity.

Raghuram G. Rajan

Putting Liquidity in Context

Liquidity is largely a function of time horizon. Timber is a long-term play for long-term buyers and liquidity matters more for short-term sellers or investors reliant on significant leverage.

In addition, investors may hold positions that are ‘effectively’ illiquid if they are too large or too small or too marginal in quality or location. When prices crash, it’s easy to blame an absence of buyers on liquidity. From this view, liquidity is a problem for poor planners.

Conclusion

The relevance of liquidity to risk, returns, or cash flow varies across investors and over time. Liquidity thrives during periods of stability and of growth. Crashes, panics, recessions, and blackouts dry up liquidity. Sizable investment assets, whether timberland or car dealerships, often comprise a diversified portfolio of smaller assets, inventories, and cash flows. The issue of liquidity is rarely all or nothing.

[1] This post includes content from the Q2 2024 Forisk Research Quarterly (FRQ) feature article, “Topics on Forest Finance: Investment Criteria and Timberland Liquidity” and from the forthcoming 7th edition of Forest Finance Simplified.

[2] “Has Financial Development Made the World Riskier?” 2005 NBER Working Paper available at: https://www.nber.org/system/files/working_papers/w11728/w11728.pdf